You’re probably familiar with IPOs, but what about SPACs? Last year saw its fair share of blockbuster IPOs from companies like Warner Music Group, DoorDash, and Airbnb. However, 2020’s staggering $50 trillion IPO story was eclipsed by the rise of the SPAC a.k.a the special purpose acquisition company. In this article we delve into the battle between SPACs vs. IPOs.

“You can think of it like: an IPO is basically a company looking for money, while a SPAC is money looking for a company” explains Don Butler of Thomvest Ventures.

Here’s everything you need to know about this increasingly popular public offering. What is it and why everyone is talking about it now? Look no further. We cover these key concepts, and use our powerful alternative data to delve into some of the most exciting public offerings.

Let’s get started with a brief look back to 2020.

The year of the SPACs

Benzinga.com called 2020 the “Year of the SPACs.” But a glance at recent filings shows that 2020 was only the beginning of their meteoric rise in popularity. More than $30 billion was raised through SPACs in the first quarter of 2021. January saw the registration of several mega SPACs, including by Fifth Wall Ventures, Intel Chairman Omar Ishrak, and Gores Group, founded by Alex Gores.

Meanwhile, office-sharing giant WeWork announced its plans to go public via a SPAC in March, after its IPO plans failed dramatically back in October 2019. As Stanford professor Michael Klausner, told the New York Times, “There have been doubts raised about [WeWork’s] business model, and those doubts may be difficult to address in an IPO roadshow.”

How does WeWork measure up against key rivals? You can check out our full analysis of the WeWork SPAC here.

SPACs are particularly appealing for cutting-edge technologies and new models backed by visionaries with a lot of money but little performance data. A recent example is Joby Aviation, the flying taxi company backed by Toyota, and Baillie Gifford, a British investment manager.

Another example is MoneyLion, a fintech platform offering mobile banking. The company merged with Fusion Acquisition Corporation in February in a deal valued at $2.4 billion, generating $500 million in gross proceeds.

SPACs vs. IPOs

A traditional IPO

An initial public offering is a major move for a private company. It permits a company to access significant funds to expand without taking on debt. In exchange for capital, the status of the company changes from privately-owned to shareholder-owned.

While global IPO activity significantly slowed at the outset of the pandemic (with a 48% volume decrease in April and May compared to the same period in 2019), appetite quickly recovered. In fact, according to Baker Mackenzie, 2020 saw the highest IPO capital raising activity in a decade.

How do IPOs work?

- A private company decides to sell shares to the public.

- Following an audit of its financials, paperwork is filed with the SEC.

- The stock exchange reviews the company’s application to conduct an IPO, which can be accepted, amended, or rejected.

- With all approvals in hand, the company defines the number of shares it will sell on the selected stock exchange. An investment bank determines the IPO price based on its evaluation of the business.

- The initial share price is listed and released, and the stock is now available for public trading.

Special purpose acquisition company (SPAC)

In contrast to an IPO, a SPAC is essentially a shell company that serves no purpose other than to raise investor capital to acquire an existing business and take it public. That’s why it is also known as a blank check company. SPACs work in the reverse order of an IPO. Rather than a company selling shares to public investors, the SPAC goes public on the stock market by selling shares to investors. It then tries to acquire a company before the two-year deadline.

How do SPACs work?

- A team of high-profile investors such as hedge funds or private equity heads and industry leaders create a SPAC. The management team is known as the ‘SPAC sponsors.’

- The SPAC raises capital from investors via a roadshow or other outreach efforts, typically trading at around $10 per share.

- The money is deposited into an interest-bearing trust account.

- In the meantime, the SPAC sponsors research the market, looking for a private company seeking to go public via acquisition.

- Once identified, all SPAC shareholders must agree to the deal, which is often structured as a reverse merger. This means that the operating company merges with and into the SPAC or a subsidiary of the SPAC.

- After the acquisition, SPAC shareholders have the option to redeem their shares in return for their initial investment or exchange their SPAC shares for shares in the acquired company.

- The SPAC sponsors must identify a suitable company within around two years after initiating the IPO. If unsuccessful, the SPAC is liquidated, and shareholders receive their initial investment plus interest.

- However, if the deal is successful, the SPAC sponsors have the opportunity to snap up 20% of the company (potentially worth millions of dollars) for just $25,000. This reward is dubbed the ‘promote’ and can be very lucrative for the sponsors.

- All SPACs must register with the SEC.

Discover more investor terms to help you understand alternative data

IPO pros and cons

SPACs vs IPOs: IPO Pros

IPOs offer increased visibility. A listing on the stock exchange dramatically improves a company’s visibility, signaling its success and growth potential. A successful IPO can be used as leverage to gain better terms when the company applies for loans.

Investors get in early. For investors, it’s a chance to get in on the ground floor of a growing company. The investment can generate healthy returns, even in the short term.

Long-term gain is significant. The potential for long-term gains is also substantial. Consider this: When Facebook (FB) went public in 2012, its stock opened at just $38 per share. Now, shares of the social media giant sare trading at $257 per share – a 576% increase (not bad).

The IPO process is transparent. The share price is revealed in the IPO documents for all investors to review in advance.

It’s affordable. Emerging companies typically discount the opening share price, making it very affordable for investors. For example, when Amazon (AMZN) went public in 1997, its share price was just $18.

SPACs vs IPOs: IPO Cons

The process is expensive and time-consuming. The company must retain an investment bank, and company executives lose considerable time completing all the paperwork and requirements. The costs of a traditional IPO include the investment banks, legal, and auditing fees.

Loss of control comes with the territory. Entrepreneurs and company owners lose control of the business after an IPO. They now have a Board of Directors with the authority to change the founding team.

The risk for investors is higher. IPOs are riskier for investors compared to established stocks and blue-chip stocks that have already demonstrated years of steady performance.

Share prices are more volatile. There is the real potential that prices will plummet after the IPO, leaving investors with shares that are worth far less than the IPO price. A perfect example of this is with the ride-hailing service Lyft (LYFT). Shares of LYFT plummeted 22% on its second trading day from the opening day’s intraday high. Now, almost two years later, Lyft is still trading down 21% vs. its $72 IPO price.

Looking for IPO insights? Get started now

SPAC pros and cons

SPACs vs IPOs: SPAC Pros

The process is cheaper, quicker and easier for companies. One of the benefits of a SPAC vs a traditional IPO is that a SPAC merger enables a company to access the capital they need quickly and affordably.

Experienced SPAC sponsors help companies. Steve Fletcher, CEO of Explorer Acquisitions, an advisor and backer of SPACs, tells Forbes: “With the recent proliferation of SPACs, we believe that investors will increasingly focus on SPACs that have deeply experienced and talented operating executives. These executives can truly help companies after the SPAC business combination.”

Investors can redeem shares. Crucially, SPAC investors can redeem their shares (for their $10 purchase price plus interest) if they disapprove of the proposed acquisition.

Projections are forward-looking. One of the benefits of SPACs vs IPOs is that SPACs permit companies to provide future forecasts. This is not allowed in a traditional IPO prospectus because of liability risk. Since a SPAC is, in essence, a merger, they can inform investors of what the company will look like post-merger.

Plus:

There’s more opportunity for investors. Market instability has pushed SPACs to the forefront. Entrepreneurs worry that the traditional IPO route might harm their first attempt to go public. They can postpone and wait for the market to calm down or merge with a SPAC. Many are choosing the latter.

Expect more certainty. Unlike IPOs, the SPAC and the target company first agree on a fixed valuation. This process limits price volatility once the SPAC starts trading shares. However be aware that the SPAC may receive a lower valuation than it would from an IPO and it must also pay the sponsor fee.

SPACs vs IPOs: SPAC Cons

Investors have blind spots. When investors buy into the SPAC’s IPO, they don’t know the final acquisition target. Investors must rely on the SPAC’s founders and managers to pick the best target company.

As the SEC states, “If you invest in a SPAC at the IPO stage, you are relying on the management team that formed the SPAC…. A SPAC may identify in its IPO prospectus a specific industry or business that it will target as it seeks to combine with an operating company, but it is not obligated to pursue a target in the identified industry.”

Delay in returns are par for the course. Another downside of a SPAC is that SPAC managers have two years to find and begin the process of acquisition. Even though investors ultimately receive money plus interest, they have lost the potential returns from a couple of years of actively investing on the stock market.

Beware of conflicts of interest. The two-year deadline can also create a conflict of interest. Due to the sponsor promote “SPAC founders are very incentivized to do a deal,” Matt Kennedy, of Renaissance Capital, told the WSJ. “Investors shouldn’t rely on their due diligence.” At the same time, the investor holding is diluted once the SPAC founders collect their 20% stake.

Historically, returns are weaker. Of the 313 SPACs IPOs since the start of 2015 to October 2020, 93 completed mergers and took a company public. Of these, Renaissance Capital calculated that the common shares delivered an average loss of -9.6% and a median return of -29.1%, vs. the average 47.1% return for traditional IPOs in that period. Only 29 of the SPACs in this group (31.1%) had positive returns, according to Renaissance Capital.

FYI, this isn’t necessarily the case. Returns for some recent SPAC mergers – like Virgin Galactic, Luminar, and DraftKings – have been impressive.

High-profile IPOs in 2020

According to Statista, there were 407 IPOs in 2020, twice as many as in the previous year. Some of the most prominent IPOs of 2020 include:

- Software developer Snowflake (SNOW) earned the title of largest software IPO of 2020, raising $3.4 billion. Its share price jumped 104% on its first day of trading in September. Starting at $120, investors climbed on board, quickly doubling the price.

- DoorDash (DASH), which earned the ranking of 2020’s third-largest IPO. Going public in December, its shares surged by 80% within the first day of trading on the New York Stock Exchange (NYSE). The company’s valuation rose to $60B. Check out our analysis of the DoorDash IPO here.

- Unity Software (U) is a platform for creating and operating interactive, 3D content. It also debuted in September, raising $1.3 billion as its opening share price surged by double-digits.

- Airbnb (ABNB) also debuted in December on Nasdaq, but its reception was more muted. Opening at $146 per share, ABNB rose to a high of $165 and then fell to $124 three days later, dropping 25%. Shares have now recovered to $196 after Q4 results came in better-than-feared.

IPO trends for 2021

In 2021 there’s a lineup of mega IPOs yet to hit the market, indicating that 2021 has the potential to outshine even 2020. Already this year, dating app Bumble (BMBL) went public with a $2.2 billion initial public offering on Feb. 11, 2021. Shares spiked by 63% on the first day of trading, doubling the capital it had anticipated.

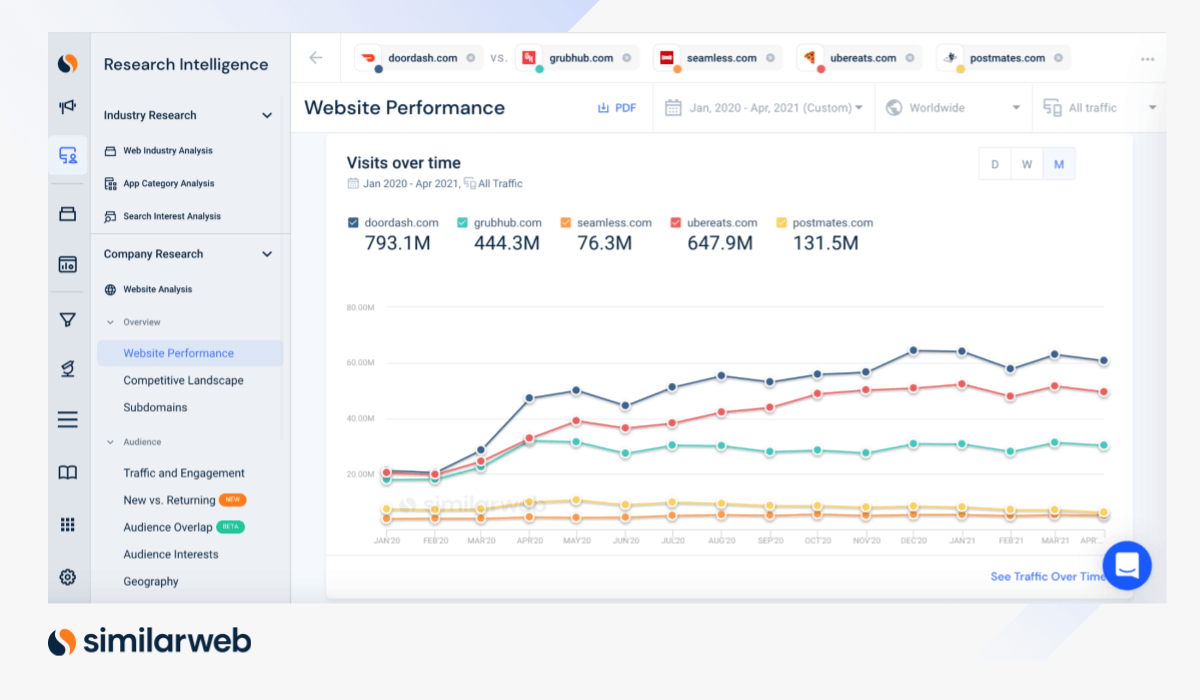

Looking forward, we’re keeping our eye on trending companies such as Instacart, a grocery pickup and delivery service, that has retained Goldman Sachs to manage its IPO. The company experienced phenomenal growth during 2020 as global lockdowns drove home delivery demand through the roof. However, as lockdowns ease, the company’s online traffic growth has slowed:

In the week of June 4 2021, visitors to instacart.com were down 20% on a year-over-year basis.

Also in the line-up is the digital payments company, Stripe and possibly SpaceX, founded by Elon Musk. And of course, all eyes are one Robinhood, the hugely popular retail brokerage platform, which is expected to go public later this year.

Download the Robinhood IPO Analysis

Download the full Robinhood analysis

Personal info

In a recent Goldman Sachs’ report, Jay Ritter of the University of Florida, sums up the IPO outlook: “I expect the volume of IPO activity will remain high as long as the stock market continues to perform well. The IPO market has always been hyper-sensitive to stock market movements, and so if the stock market takes a dive like it did last February, the IPO market would likely shut down pretty rapidly. While that’s possible, the more likely scenario is that reasonably high volumes will continue and maybe even grow.”

And what about SPAC trends?

According to SPAC Research, SPACs are increasing. In 2013, there were 10 SPACs with roughly $144.7 million in assets. Recent data reveals that almost 200 SPACs went public in 2020 and raised more than $70 billion, nearly matching 2020 IPO performance. Consider these examples:

- In September, real estate tech company Opendoor (OPEN) announced its intention to go public via a merger with Social Capital Hedosophia II, a SPAC managed by Chamath Palihapitiya. It became a public company debuting on the market in December. Opendoor raised roughly $1 billion in cash from the transaction.

- Richard Branson’s Virgin Galactic (SPCE) merged with Palihapitiya’s SPAC in late 2019, allowing the company to go public and gain a $2.3 billion market capitalization. Virgin Galactic’s share price rose by 45% from its debut.

- Nikola (NKLA) was one of the first high profile electric-vehicle companies to go public via a SPAC listing. It merged with VectoIQ Acquisition Corp, backed by ValueAct and Fidelity. After the merger, the company’s valuation rose to almost $28.8 billion, despite its lack of revenue.

- DraftKings (DKNG), launched as a fantasy sports company in 2011. It merged with Diamond Eagle Acquisition Corp, netting the sports betting company a valuation of $2.7 billion. The company went public in April with an initial share price of $17, which rose to $52.11 a few months later.

A new type of SPAC

Hedge fund activist Bill Ackman of Pershing Square launched a unique $4 billion SPAC in July 2020. The price per share was $20, higher than the usual $10 – but his takeaway is 0%. In one fell swoop this eliminated the risk of shareholder dilution, while also removing the founder incentive to complete a deal before the deadline.

SPAC trends in 2021

Turning to 2021, SPACInsider reports that more than $38 billion has been raised by SPACs since the beginning of the year, almost half the total amount raised in 2020.

For instance, Anne Wojcicki, CEO of 23andMe, a consumer genetic-testing company, announced in February her intent to go public through VG Acquisition, a SPAC founded by Richard Branson. They each will contribute $25 million to the SPAC and expect to raise $759 million from private and public investors to fund the acquisition of 23andMe. For Wojcicki, it mattered that she would know who her investors are in advance, unlike with an IPO when going public comes first.

On the other hand, David Solomon, CEO of Goldman Sachs, recently warned that the current SPAC boom may have ‘gone too far.’ Speaking to investors in mid-January 2021, Solomon noted flaws in the current SPAC ecosystem that require more time to repair before becoming a sustainable mechanism for raising capital.

He believes that the market’s condition may have pushed companies to turn to SPAC acquisition because they had no other alternative. If the environment changes, SPAC activity could decline. “The ecosystem is not without flaws,” he said, according to the Financial Times. “I think the incentive system is still evolving. One of the things we’re watching very, very closely is the incentives for the sponsors and also the incentives of somebody that’s selling.”

SPARCs

From SPACs to SPARCs. Bill Ackman has also now created SPAC 2.0 aka the SPARC – a special purpose acquisition rights company. He will seek out another acquisition target, and if investors approve of the prospective deal, they can cough up the requisite cash. In other words, the funding only comes after the target has already been found.

How will direct listings impact IPOs and SPACs?

A new factor in the IPOs vs. SPACs mix is the Securities and Exchange Commission’s (SEC) recent rule change regarding direct listings. At the end of 2020, the SEC approved the NYSE’s proposal for a new type of direct listing that allows companies to issue new shares and sell them directly to the public on the first day of trading.

Commissioner Elad Roisman explained that primary direct listings enable companies to offer their shares to the public efficiently and fairly while protecting investors. Indeed, direct listing provides many of the benefits of a traditional IPO, such as the ability to raise capital on the public markets, and use publicly traded shares as acquisition currency.

However, the direct listing approach isn’t appropriate for every company. It does eliminate the need to work with an investment bank, broker, or underwriter, but a company needs to have a well-established profile to make it work. Brands such as Spotify (SPOT) and Slack Technologies (WORK) enjoyed successful direct listing because they already had a large following.

In 2020, both Asana (ASAN) and Palantir (PLTR) both also chose to go public via this innovative new approach. And following in their footsteps, the cryptocurrency trading platform Coinbase has just opted to go public via a direct listing. Coinbase shares are now available for trading on NASDAQ under the ticker COIN. However the stock dropped 20% in May 2021 as crypto volatility sparked a COIN selloff.

Download our full analysis for more on Coinbase Wallet and Coinbase for financial institutions

Download the full Coinbase analysis

Personal info

Conclusion

All indicators point to a healthy market in 2021, with growing demand for both IPOs and SPACs. With the groundbreaking deals taking place in the SPAC space lately, it seems unlikely that this trend will die down anytime soon.

As Goldman Sachs’ David Ludwig writes: “many aspects of the traditional IPO process still appeal to a broad set of companies. It’s a tried-and-true process, and many companies feel that they have more control over the outcome. I expect that the majority of new listings will take place via the traditional IPO route, but I also think that SPACs and direct listings will comprise a materially larger share of public listings over time.”

What will be most interesting is to see how SPACs evolve going forward. For instance, will the balance of risk/reward for investors vs. the management team improve? And will SPARCs take over from SPACs? In the meantime, you can follow key digital data trends for companies on the cusp of going public using the Similarweb platform. And you can track upcoming IPOs here.

Discover key data points for 1000s of companies – It’s free!

Investor Insights Manager

Harriet, a Cambridge graduate and qualified U.K. lawyer, transitioned from metal market journalism to financial blogging, using digital data for investment insights.

Related Posts

Invest using the most insightful digital alt data

Leverage data used by 5,000+ companies to improve your strategy